Prices for goods like housing, tuition, and oil appear to skyrocket or fluctuate wildly in dollars, but they often remain stable or even decrease when measured in gold.

Although nominal wages and stock market indexes have reached historic highs, workers’ actual command over real resources has eroded when evaluated against gold.

Because gold cannot be printed or altered by central bank policies, it serves as an independent measuring stick that exposes the long-term effects of fiat currency intervention and inflation.

Viewing the economy through “gold lenses” reveals that apparent financial growth is often just a reflection of the changing value of the dollar rather than a true increase in wealth.

For most people, gold occupies one of two conceptual categories. It is viewed either as a hedge/investment or as a historical monetary asset – something associated with central banks, long-term wealth preservation, and earlier monetary systems. Yet there is another, arguably more useful way to think about gold: not merely as an asset, but as a lens.

Looking at the world through “gold lenses” does something curious. It alters our perception of prices, wealth, inflation, and even economic policy itself. Objects and services that appear dramatically more expensive over time can sometimes look surprisingly stable, or even cheaper, when measured in ounces of gold. Meanwhile, what appears to be prosperity in nominal terms may look rather different when evaluated in terms of enduring purchasing power.

This way of viewing the world starts with a simple question: instead of asking what something costs in dollars, euros, or yen, what if we asked what it costs in gold?

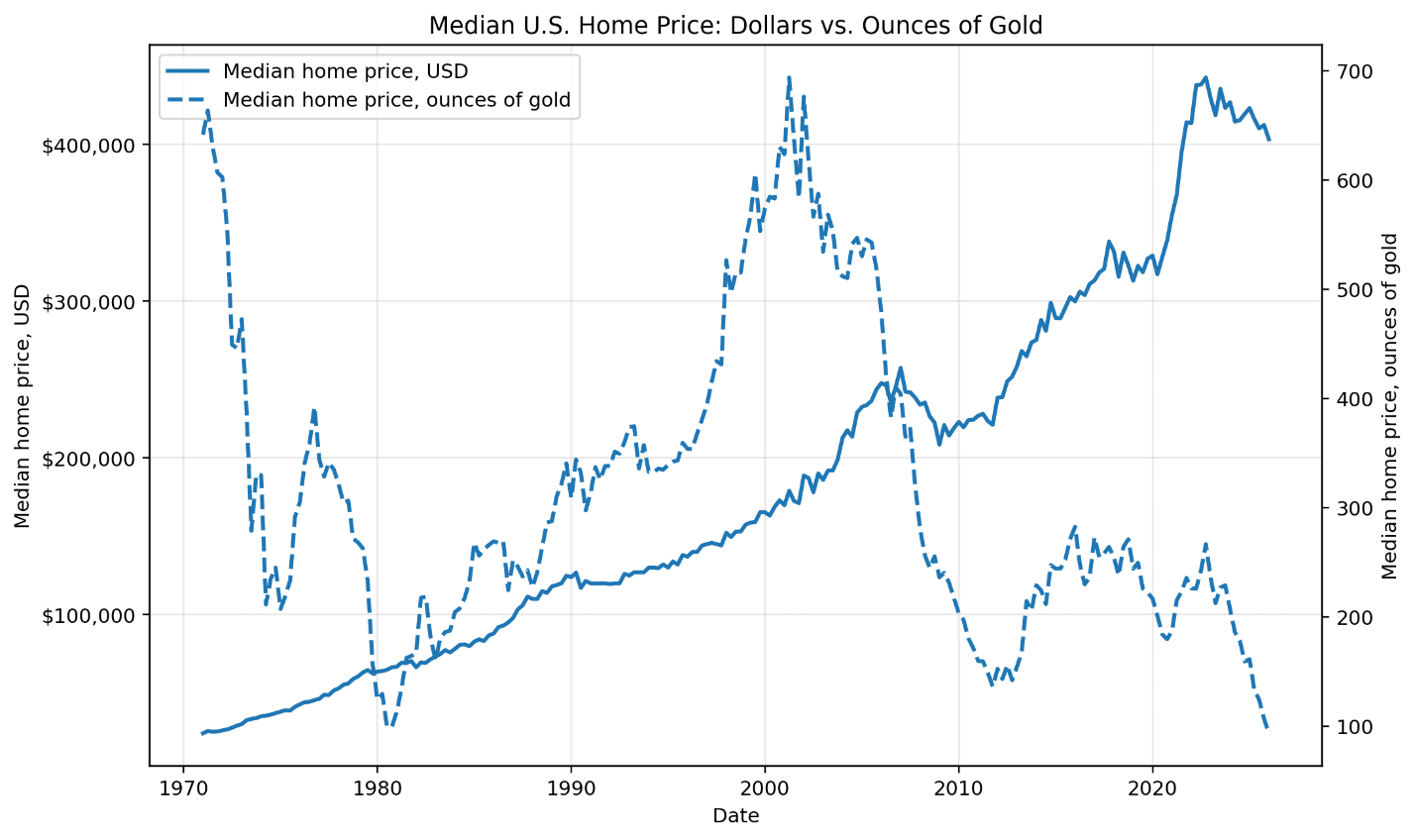

Consider housing. Americans rightly lament that homes have become vastly more expensive over time. In nominal dollar terms, they certainly have. A median American home that cost roughly $122,000 in 1990 now costs well over $400,000, seemingly confirming a story of runaway unaffordability. But gold lenses complicate that story. In 1990, the median home required roughly 320 ounces of gold to purchase. By the housing bubble era of 2000, that figure had risen to more than 600 ounces, reflecting both rising home prices and depressed gold valuations. Yet by 2025, despite median home prices reaching approximately $415,000, the same home required only about 119 ounces of gold. Housing became dramatically more expensive in dollar terms while becoming considerably cheaper in gold terms: not because homes suddenly became affordable, but because the denominator changed.

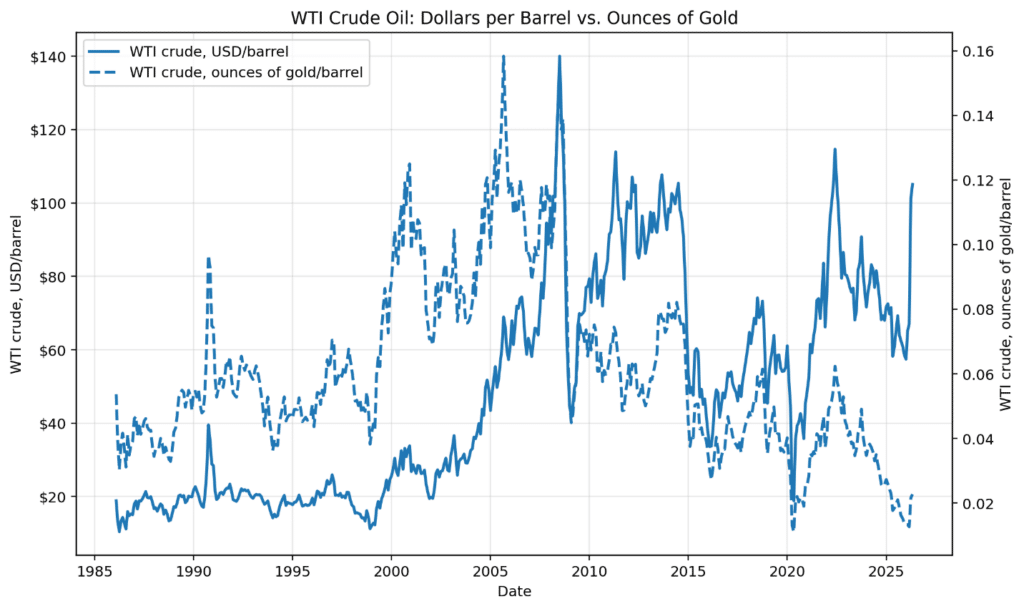

The same phenomenon appears elsewhere. Oil, food, automobiles, luxury watches, and even higher education tell different stories when denominated in gold. Crude oil, for example, appears wildly volatile in dollar terms, moving from around $25 per barrel in 1990 to more than $100 today. Yet in gold terms, the swings look far less dramatic: a barrel of oil required about 0.06 ounces of gold in both 1990 and 2010, compared with only around 0.02 ounces in recent years. What often appears to be commodity instability may sometimes reflect instability in the currency doing the measuring.

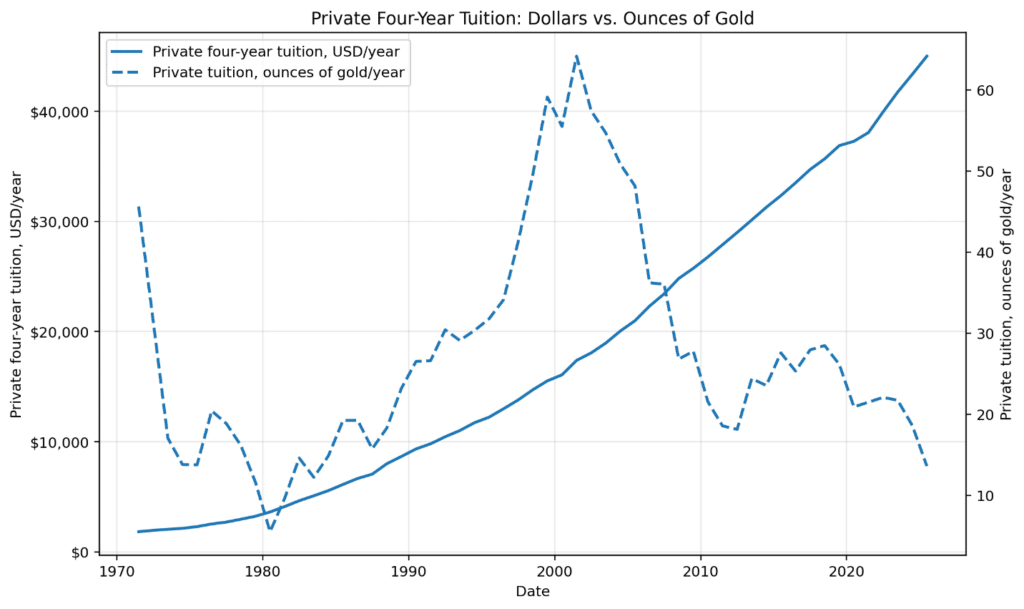

Even college tuition – a frequent symbol of modern costs run amok – looks different through gold lenses. Private four-year tuition rose from roughly $9,300 annually in 1990 to around $45,000 today, but measured in gold, tuition peaked near 58 ounces in 2000 and stood closer to 13 ounces by 2025. That does not, of course, mean that college became inexpensive. Rather, it reminds us that nominal prices can exaggerate long-run changes when money itself is changing value.

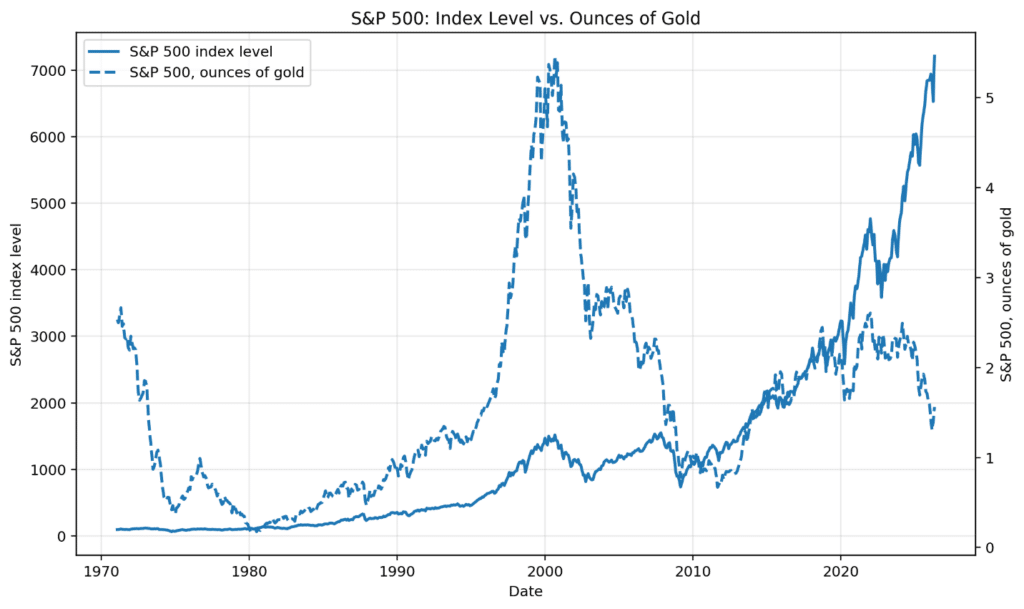

Even financial markets tell a different story through gold lenses. Investors obsess over whether the Dow Jones Industrial Average or S&P 500 has reached new highs, but nominal records can be deceiving. At the height of the dot-com boom in 2000, the S&P 500 traded near 1,420, equivalent to roughly 5.1 ounces of gold. By contrast, in 2025, despite the index exceeding 6,200, it represented only about 1.8 ounces of gold. Investors may possess substantially more nominal wealth than they once did, but their command over scarce monetary resources may not have expanded nearly as dramatically. Economic life is not ultimately experienced in brokerage statement balances or stock index points but in purchasing power exchanged for real goods and services over time.

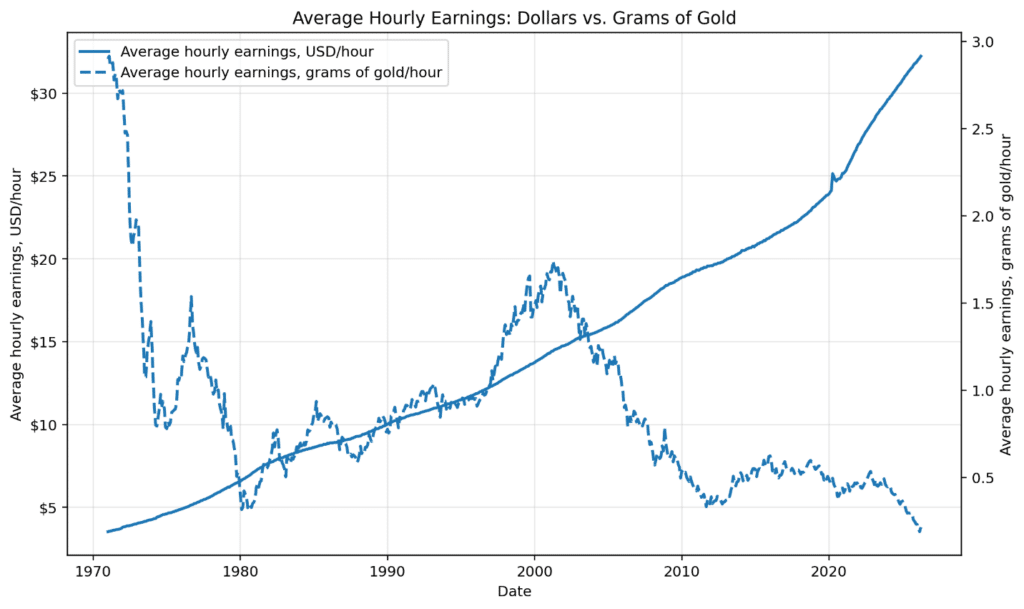

Wages reveal a similarly complicated story. Average hourly earnings rose from roughly $10 per hour in 1990 to more than $31 today, seemingly an impressive gain. Yet measured in gold, an hour of labor purchased approximately 0.027 ounces of gold in 1990, compared with only about 0.009 ounces today: roughly 0.84 grams of gold per hour then versus 0.28 grams now. Nominal wages have risen dramatically. Yet measured against a hard monetary benchmark, workers’ command over real resources has deteriorated.

This is where gold becomes more than a hedge against uncertainty or purchasing-power erosion. It can be used as a diagnostic tool – a way of observing the cumulative effects of interventionism on money itself.

Modern fiat (unbacked) currencies are products of institutions and policy choices. Central banks adjust interest rates, governments run deficits, emergency spending proliferates during crises, and financial systems are repeatedly backstopped through interventions designed to prevent disorder. Many of these actions may be understandable in the moment. Yet they also alter the purchasing power of money over time. Because fiat currency is elastic by design, its quantity and cost can be influenced by policy in ways impossible under a harder monetary standard.

Gold, by contrast, tends to sit outside these interventions. It has no central bank, no earnings calls, no quarterly guidance, and no committee meeting determining whether more should exist next month. Its supply grows slowly and imperfectly, constrained by geology, extraction costs, and physical reality. That makes it an unusually useful measuring stick for long-term comparisons.

Looking through gold lenses therefore reveals something often obscured in conventional discussions of inflation. Inflation is not merely a rise in consumer prices; it is also a reflection of changes in the value of money itself. When a cup of coffee costs twice as many dollars as it once did, part of the story may involve wages, scarcity, labor, or quality improvements. But part also reflects what has happened to the purchasing power of the US dollar.

Seen this way, gold offers a perspective on economic interventionism not through ideology, but simple observation. One need not believe every monetary expansion is catastrophic or every government program misguided to recognize that decades of fiscal deficits, central bank balance sheet expansions, emergency lending facilities, and recurring crises leave fingerprints on currency values. Gold, over long periods, often captures those fingerprints more clearly than nominal prices alone.

None of this means that gold is perfect. Nor does pricing the world in gold solve the practical reality that we live in dollar-denominated economies. Salaries are paid in dollars, taxes collected in dollars, mortgages serviced in dollars, and grocery bills settled in dollars.

Still, there is intellectual value in periodically stepping outside the “fiat frame.” Looking at the world through gold lenses can expose how much of what we perceive as rising prosperity is nominal rather than real, how much apparent price instability reflects monetary instability, and how intervention in the financial system accumulates consequences over time.

For much of history, gold served simultaneously as a medium of exchange, a store of value, and a unit of account. Prices were quoted in terms of gold itself, not currencies redeemable only by confidence and legal tender laws. That world is gone, at least for now. Whatever one’s views on whether it should return, there is little evidence that advanced economies are likely to re-anchor themselves to gold anytime soon.

Until or unless that changes, we will continue to live in a fiat world, navigating its opportunities and distortions alike. In such a world, gold may not tell us what to do, nor does it offer a promissory answer to every financial question. But it can help us protect ourselves against uncertainty, shield against falling purchasing power, and tell us something valuable: what our money, and the policies shaping it, have quietly been doing all along.

About the author: Peter C. Earle, Ph.D, is the Director of Economics and Economic Freedom and a Senior Research Fellow who joined AIER in 2018. He holds a Ph.D in Economics from l’Universite d’Angers, an MA in Applied Economics from American University, an MBA (Finance), and a BS in Engineering from the United States Military Academy at West Point.

Prior to joining AIER, Dr. Earle spent over 20 years as a trader and analyst at a number of securities firms and hedge funds in the New York metropolitan area as well as engaging in extensive consulting within the cryptocurrency and gaming sectors. His research focuses on financial markets, monetary policy, macroeconomic forecasting, and problems in economic measurement. He has been quoted by the Wall Street Journal, the Financial Times, Barron’s, Bloomberg, Reuters, CNBC, Grant’s Interest Rate Observer, NPR, and in numerous other media outlets and publications.

Disclaimer: All opinions expressed by the author are the author’s opinions and do not reflect the opinions of Goldco. The author’s opinions are based on the author’s personal experience, education and information the author considers reliable. Goldco does not warrant that the information contained herein is complete or accurate, and it should not be relied upon as such.

3 Key Points to Consider Growing economic uncertainty and market volatility has many people wondering how to help preserve their wealth More and more people are looking to help...

Key Takeaways The historic 15-to-1 or 16-to-1 gold-to-silver ratios were artificially set by legal tender acts and bimetallic government policies rather than discovering fundamental market...

Gold IRAs are retirement accounts that allow you to help protect your wealth through ownership of physical gold coins or gold bars Gold IRAs can be funded through tax-free rollovers from...

*Applies only to qualified orders. Get up to 5% back in FREE Silver when you purchase $50,000 – $99,999 in Goldco premium coins. Get 10% in FREE Silver when you purchase $100,000 or more in Goldco premium coins. Cannot be combined with any other offer. Additional rules may apply. Contact your representative to find out if your order qualifies. For additional details, please see your customer agreement. Goldco does not offer financial or tax advice regarding the purchase of precious metals.

About the author:

About the author: