Gold and the Long Bond: Why the Old Relationship Is Fraying

Written by Peter C. Earle, Ph.D

Share |

5min read

Key Takeaways

The historical inverse relationship between gold prices and real interest rates has frayed.

Rising Treasury yields are no longer just seen as competition for gold ; they are interpreted as a signal of growing fiscal strain, mounting federal debt, and diminished political consensus for fiscal restraint.

Central banks, particularly in emerging markets like China and India, have become major buyers to protect reserve assets from Western political vulnerabilities and sanctions risk.

Gold’s role has evolved from being a simple inflation hedge into a “trust or credibility hedge,” serving as monetary ballast for those seeking insulation from eroding confidence in long-term government, fiscal, and institutional stability.

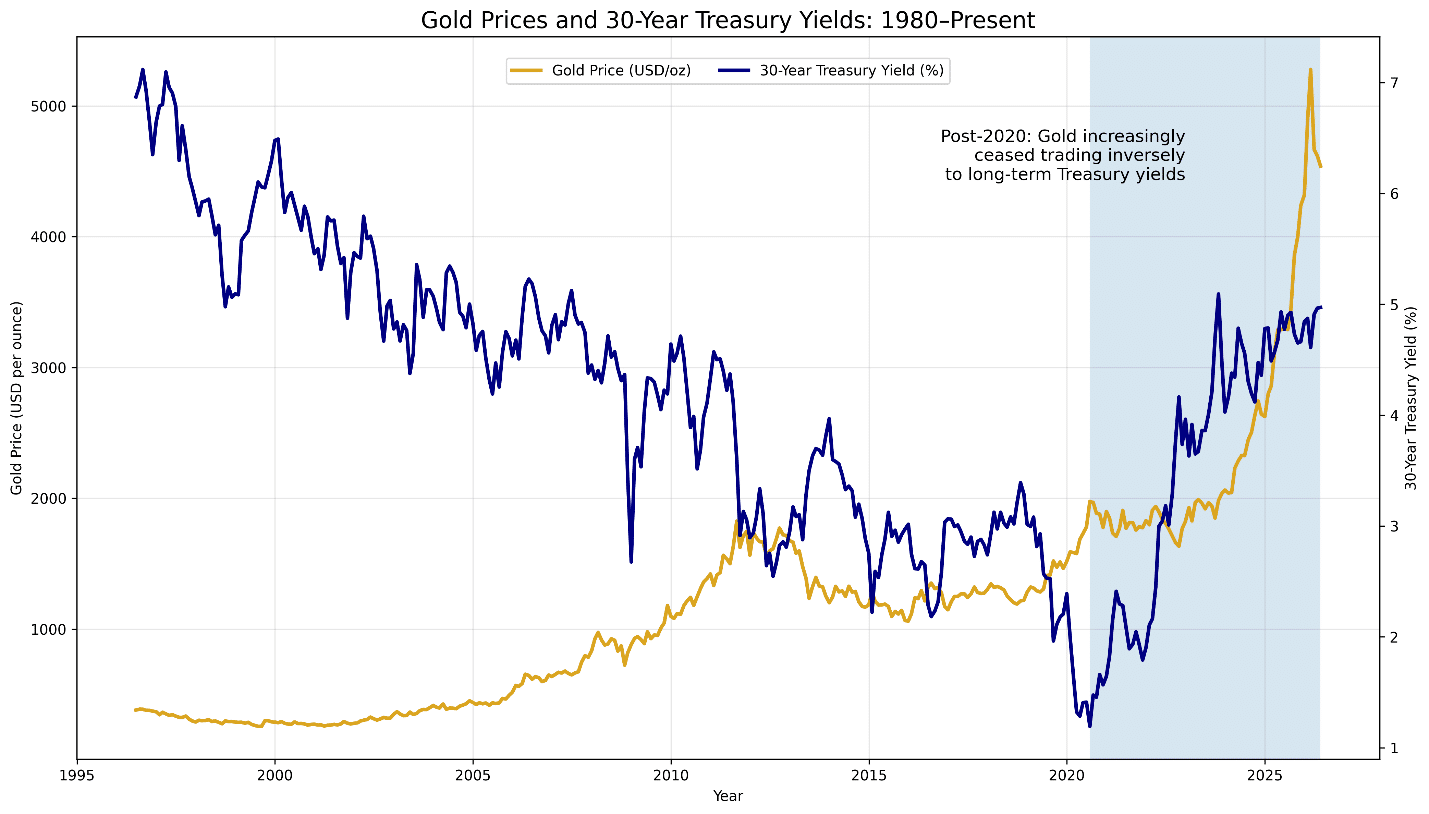

For decades, one of the most reliable relationships in finance was the inverse connection between gold prices and real interest rates. The logic was straightforward: gold yields nothing. When buyers could earn attractive inflation-adjusted returns on safe government debt—especially long-dated US Treasuries – the opportunity cost of holding gold increased, typically weighing on prices. Conversely, when real yields fell, gold became relatively more attractive, often appreciating as buyerrs sought protection against inflation, currency weakness, or monetary instability.

Yet over the last several years, and especially within the last few months, something unusual has occurred. Gold has remained historically elevated even as real yields, particularly on long-duration US government debt, have stayed stubbornly high. The yield on the 30-year Treasury has hovered near levels not seen consistently in years, while inflation-adjusted rates remain positive and, at times, historically elevated. Under the traditional framework, gold should be under pressure. Instead, it has proven remarkably resilient.

Perceptions of Sovereign Risk and Fiscal Strain

What explains this apparent breakdown? One answer lies in changing perceptions of sovereign risk; not default risk in the conventional sense, but concerns about fiscal sustainability and long-term monetary credibility. Investors increasingly confront a paradox: US Treasury securities remain the world’s benchmark safe asset, yet America’s debt trajectory appears increasingly difficult to ignore. Federal deficits remain elevated even during periods of economic expansion, debt servicing costs have surged alongside higher interest rates, and political consensus around fiscal restraint has vanished from the political conversation.

This creates an unusual dynamic. Rising Treasury yields would ordinarily compete with gold by offering investors greater returns. But if those same higher yields are themselves interpreted as evidence of growing fiscal strain – reflecting concerns over mounting Treasury issuance, debt rollover risks, or long-term inflationary pressures – they may simultaneously strengthen the case for holding gold. In other words, rising yields may no longer purely represent competition for gold; they may increasingly signal the very instability gold buyers seek protection against.

The Rise of Central Bank Demand and Geopolitical Realities

A second factor involves the changing composition of gold demand. Traditionally, Western institutional investors, hedge funds, and retail flows through exchange-traded funds played an outsized role in gold pricing. Increasingly, however, central banks – particularly in emerging markets – have become major buyers. Countries such as China, India, Turkey, and others have steadily accumulated gold reserves in recent years.

The motivation is not difficult to understand. Following the freezing of Russian foreign reserves after the 2022 invasion of Ukraine, many governments were reminded that reserve assets held within the Western financial architecture can become politically vulnerable. Gold, by contrast, carries no issuer risk, no sanctions risk, and no counterparty risk. It is among the few internationally recognized reserve assets that exists outside the liabilities of another government.

This shift matters because central bank buying tends to be less sensitive to short-term changes in yields than speculative investor flows. A pension fund manager deciding between Treasuries and bullion may care deeply about inflation-adjusted returns; a sovereign reserve manager concerned about geopolitical fragmentation may care far less.

Evolving Psychology: Gold as a Credibility Hedge

There is also growing evidence that gold’s role in buyer psychology may be evolving. For years, gold was simplistically described as an inflation hedge, though the empirical relationship was sometimes inconsistent. Gold sometimes rallied amid inflation, but at other times lagged. Increasingly, gold appears less tied to inflation itself and more responsive to declining confidence in institutions – monetary, fiscal, political, or financial.

In this sense, gold is acting like what might be called a “trust (or ‘credibility’) hedge.” Investors are not necessarily buying gold because they expect imminent inflation or recession. Rather, they may be purchasing it because they feel less certain about the long-run credibility of governments, central banks, currencies, or financial blocs. A world marked by conflict, fiscal stress, repeated banking disruptions, interventionism, reserve weaponization, and debates over currency systems naturally increases gold’s appeal.

None of this means the historical relationship between gold and real yields has disappeared entirely. Higher real rates still matter, and periods of rising yields can pressure gold in the short run. Nor does any of this mean gold is destined to rise indefinitely. If inflation moderates sustainably, fiscal concerns ease, and global confidence stabilizes, gold’s momentum could flag.

But the market appears increasingly willing to tolerate something that once seemed contradictory: elevated gold prices alongside elevated long-term Treasury yields.

Conclusion

That coexistence may signal something deeper than temporary market noise. It may suggest that investors increasingly see long bonds and gold not as straightforward substitutes, but as serving different purposes altogether. One offers income and liquidity. The other offers insulation from the possibility that confidence in the broader system itself may be eroding.

In that sense, gold’s recent co-movement with long-bond yields may not represent a breakdown in the old relationship at all. Rather, it may reflect changing reasons for owning gold. In a world of rising debt, fiscal uncertainty, and geopolitical fragmentation, buyers appear increasingly to value gold less singularly as an inflation hedge and more as a form of ‘monetary ballast’ – an asset perceived as independent of politics, policy, and counterparty risk.

About the author: Peter C. Earle, Ph.D, is the Director of Economics and Economic Freedom and is Head of Research who joined AIER in 2018. He holds a Ph.D in Economics from l’Universite d’Angers, an MA in Applied Economics from American University, an MBA (Finance), and a BS in Engineering from the United States Military Academy at West Point.

Prior to joining AIER, Dr. Earle spent over 20 years as a trader and analyst at a number of securities firms and hedge funds in the New York metropolitan area as well as engaging in extensive consulting within the cryptocurrency and gaming sectors. His research focuses on financial markets, monetary policy, macroeconomic forecasting, and problems in economic measurement. He has been quoted by the Wall Street Journal, the Financial Times, Barron’s, Bloomberg, Reuters, CNBC, Grant’s Interest Rate Observer, NPR, and in numerous other media outlets and publications.

Disclaimer: All opinions expressed by the author are the author’s opinions and do not reflect the opinions of Goldco. The author’s opinions are based on the author’s personal experience, education and information the author considers reliable. Goldco does not warrant that the information contained herein is complete or accurate, and it should not be relied upon as such.

Key Takeaways The US government carries its 2615 million ounces of gold at a statutory price of $4222 per ounce (~$11 billion total), creating a massive accounting disparity against its current...

Rising national debt, dollar devaluation, and record central bank gold purchases have helped push gold prices higher over the past several years Amid persistent inflation and economic...

3 Key Points to Consider Growing economic uncertainty and market volatility has many people wondering how to help preserve their wealth More and more people are looking to help...

*Applies only to qualified orders. Get up to 5% back in FREE Silver when you purchase $50,000 – $99,999 in Goldco premium coins. Get 10% in FREE Silver when you purchase $100,000 or more in Goldco premium coins. Cannot be combined with any other offer. Additional rules may apply. Contact your representative to find out if your order qualifies. For additional details, please see your customer agreement. Goldco does not offer financial or tax advice regarding the purchase of precious metals.

About the author:

About the author: