Many Americans today have become 401(k) millionaires thanks to the recent performance of stock markets. But while markets may be flying high today, that won’t always be the case.

When the next market crash comes, there will be some people who will have prepared themselves ahead of time, helping protect themselves from loss. But there will be others who haven’t prepared, and who find themselves staring down massive losses as a result.

Wealth protection can be critical during economic downturns, helping to mitigate losses through asset diversification and other strategies. And preparation for that wealth protection begins before markets turn south.

That means that strategies that reap rewards during a bull market may be ditched during a recession. And many people will gladly hold onto assets that don’t change value at all rather than risk losing money during a recession.

What you choose to do, and which assets you choose to hold, are largely determined by your appetite for risk and your overall financial goals. But there are two assets that have remained incredibly popular as safe havens during recessions and times of financial turmoil: silver and cash.

Both silver and cash have their benefits and drawbacks, and each can play a role in protecting your wealth against loss. So which is better for you as a safe haven asset: silver or cash?

Silver vs. Cash Historically

70 years ago we wouldn’t have even had this conversation, because silver was cash. Older Americans still remember the days when silver quarters, half dollars, and dimes were used in everyday commerce.

Even many of the bills used as money were redeemable in silver on demand. But that all began to change in the early 1960s.

As the market price of silver began to rise, the silver content of circulating coinage began to be worth more than the coins’ face value. And so silver coinage began to be pulled out of circulation and melted for its metal content.

This led to a shortage of coinage, and so in 1964 the US government decided to switch its subsidiary coinage to cupronickel starting in 1965. Once that switch occurred, silver coinage disappeared from circulation virtually overnight.

And this wasn’t something limited to the United States either. European countries, many of whose silver coins contained less silver than US coinage, also began facing the same pressures, so that by the mid-1970s most silver coinage was out of circulation around the world.

Even the silver certificates in the US were eventually no longer redeemable in silver, with the promise of silver redemption being revoked in 1968. Since then, silver hasn’t been cash but rather an alternative to cash.

For many Americans, buying and owning silver retained its allure. Yet many others chose to move forward with cash.

Advantages of Cash

Cash has many advantages. Here are four important ones.

Wide Acceptance

Speed of Use

Portability

Anonymity

Wide Acceptance

One of the major advantages of cash is its wide acceptance and anonymity. Go anywhere in the country and you can use cash to buy things. Even with the growing use of credit cards and electronic payments, there are very few businesses that don’t accept cash.

With the rising cost of credit card processing, many businesses will even offer you a cash discount if you pay in cash. And if you ever need to buy something from an individual, just about everyone will accept cash as payment.

Speed of Use

Cash payments are instant. As soon as money changes hands, the transaction is done.

There are no funds to be cleared by banks behind the scenes, no credit card bills to pay every month. Cash payments settle instantly.

And if you rely on cash as your primary source of spending, it can also help you stick to your budget. Once your cash is gone, you can’t spend anymore, thus limiting your ability to overspend.

Portability

Cash is also easily portable, and a wallet can fit thousands of dollars in it. Inflation is slowly eating away at the value of the $100 bills we have, but you can still fit enough money into your wallet to purchase a huge amount of food, a major appliance, or even a cheap used car.

Anonymity

One of the major advantages of cash is its anonymity. There is no record of any purchase or sale using cash, nor does either party have to know the other’s identity.

While some people or entities may abuse this for nefarious purposes, it has many benefits for the average American who would rather not see his purchases aggregated, analyzed, and sold by private corporations to advertisers and government agencies.

The war on cash is an effort to eliminate this anonymity and make every financial transaction transparent to the government. That’s one reason that many people today distrust efforts to push electronic payments.

Disadvantages of Cash

Of course, everything has its disadvantages as well as its advantages. Here are some of cash’s disadvantages.

Security and Loss

Bulk

Health Concerns

Counterfeiting

Inflation

Security and Loss

Like anything else you own, cash is at risk of getting stolen. And the more cash you have, the worse the theft of it will be.

If you have large amounts of cash at home, you’re probably worried that it could get stolen at any time. And the same goes for carrying large amounts of cash outside the house too.

Storing large amounts of cash, if you choose not to use a bank or a safe deposit box, means keeping a safe handy to make sure that your cash doesn’t walk off. And even then, you’ll want to bolt that safe down to make sure it doesn’t get stolen either.

Bulk

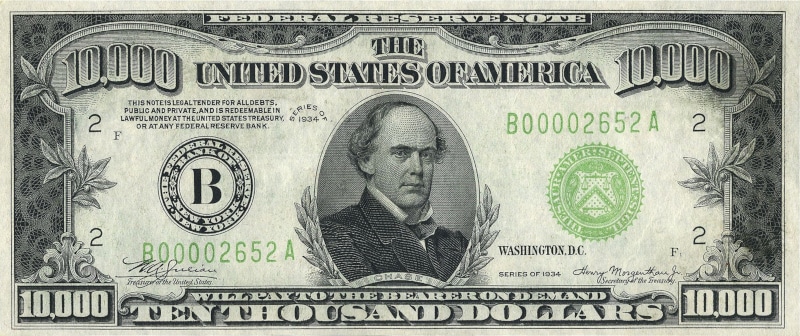

While cash is portable, carrying large amounts of it can make it impractical for large purchases. Carrying $10,000 means carrying a stack of 100 $100 bills, which would make for a big bulge in your pants.

When the Federal Reserve Act was first introduced in 1913, the US Treasury was required to print $10,000 notes in such quantities as were necessary to supply the Federal reserve banks. That statute is still on the books, but Treasury has long since ceased producing those bills, as the government is trying to cut down on tax evasion and money laundering.

But that $10,000 bill today has as much purchasing power as $312.55 did in 1913. So while it may seem like a lot, it’s actually not really.

With the way inflation is going, there may eventually be a time when $100 bills are used like $5s and $10s are today. And when that happens, the utility of cash could be greatly diminished.

Health Concerns

You’ve probably heard stories of studies that find traces of cocaine on over 90% of bills in circulation, or of the germs that can catch a ride on cash. It became a real fear during COVID, when many people thought they might be able to catch COVID from handling cash.

While these fears may be slightly overblown, there’s still a bit of a stigma attached to dirty, used bills. And if the thought that the money in your wallet may have spent time in a strip club or been used to snort cocaine makes you feel ill, cash may not be for you.

Counterfeiting

Counterfeiting remains a problem with cash, and it can be tough to tell real bills from fake ones. With counterfeiters using real banknote paper to make fakes, and with the quality of counterfeits rising, sometimes the counterfeit notes are higher quality than the real thing.

For the layman, there’s not really a foolproof way to determine real cash from counterfeits. We all just assume that the cash we use is real, and many of us try to avoid anything larger than a $20 bill for transactions.

But if you’re trying to accumulate large holdings of cash, the last thing you want to do is pick up a few counterfeits, because that calls the legitimacy of all of your cash into question.

Inflation

Inflation is the real killer when it comes to holding cash. Because of inflation, the value of your cash holdings is decreasing every year.

Even at a relatively low inflation rate of 2%, cash will lose 80% of its value over the course of your lifetime. And at the current rate of inflation, it will lose 80% of its value in less than 50 years.

The higher inflation gets, the worse it is for cash holders. If inflation were to return to levels of 10% or higher, cash would lose 80% of its value in less than 17 years.

Advantages of Silver

Many people choose to own silver as a safe haven asset, whether it’s to protect against inflation, to protect against recession-related loss, or as a potential barter method or daily use currency in a post-crisis society in which fiat currencies have collapsed.

While methods of buying silver such as purchasing silver through a silver IRA are gaining in popularity, that still requires your silver to be managed by a custodian and stored in a bullion depository. For many people, being able to hold physical silver coins or silver bars in your hands is worth it to ensure that you have your silver whenever you want it.

Here are some advantages to owning silver as a safe haven asset.

Inflation Hedge

Wealth Protection

Growth Potential

Portfolio Diversification

Familiarity

Inflation Hedge

Like gold, silver has also enjoyed a reputation for being a hedge against inflation. While the US dollar has lost 87% of its purchasing power since President Nixon closed the gold window in 1971, the silver price has risen nearly 2,000% since then.

During the entirety of the 1970s stagflation, when inflation reached into double digits, silver’s annualized rate of growth was over 30% per year, and over 20% per year even after adjusting for inflation.

Wealth Protection

Silver has been trusted to protect wealth for centuries. When currencies fail, companies go bankrupt, and governments collapse, silver is one of the first tangible, physical assets people run to for safety and security.

Growth Potential

Not only is silver popular for wealth protection, it also has the potential to make great gains during tough times. It can even outperform gold.

In the aftermath of the 2008 financial crisis, gold nearly tripled in price, but silver more than quintupled in price. Its price growth was about double that of gold.

Many people who are buying silver today believe that silver is undervalued, and are hoping that silver will once again outperform gold during the next recession.

Portfolio Diversification

Silver can help diversify your portfolio, as it alters the risk profile of your assets and can help offset losses elsewhere. How much of your portfolio you want to allot to silver may depend on your risk tolerance, aversion to losses, and overall financial goals.

Familiarity

Remember how dimes, quarters, and half dollars used to made from 90% silver? Those silver coins are now known as “junk silver,” meaning they’re purchased for their metal content, not for their collectible value.

That makes them a popular purchase for people looking to hold silver coins for a SHTF-style currency collapse. They may not be IRA-eligible silver, but they’re still popular with people who want to make direct cash purchases of silver to hold and store at home.

Disadvantages of Silver

Like everything else, silver has some disadvantages too. Here are three of them.

Storage and Theft

Counterfeiting

No Income Generation

Bulk

Storage and Theft

As a precious asset, silver will also need to be stored or protected against theft. If you’re making direct cash purchases of silver to store at home, you’ll want to make sure that you have a safe to store your silver coins in.

Since silver coins are bulkier than gold, you will likely require a larger safe if you choose to store them at home. So you’ll need to make extra sure that your safe remains out of sight of potential thieves.

If you choose to store your silver in a safe deposit box or in a bullion depository, that imposes an extra cost that can eat into any gains your silver makes. But that may be worth it to you to give you some extra peace of mind.

Counterfeiting

Silver is subject to counterfeiting too, although it’s a lot more difficult to counterfeit silver than it is to counterfeit paper currency. And the profit margins on counterfeiting silver aren’t nearly as high as they are for counterfeiting gold. Still, it’s something you have to watch out for.

Knowledgeable buyers can use calipers and scales to make sure that the silver coins they buy are legitimate, but why put yourself through the hassle? Working with trusted partners like Goldco, who work directly with mints to source silver coins, you can ensure that the silver you’re buying is 100% authentic.

No Income Generation

Silver is dependent on increases in the price of silver for its gains. That’s unlike stocks and many types of funds that offer dividends.

These dividends can contribute to compound growth over time, offering a way to build wealth—a benefit that silver does not provide.

However, when silver is growing at faster rates than overall stock markets with dividends included, is that really an issue? After all, if your goal is just to maximize your wealth, and you think silver is the way to do that, the fact that silver doesn’t pay dividends is a non-issue.

Bulk

Silver is a lot bulkier than gold, which makes it a little bulkier than cash too. A roll of 20 silver half dollars, for instance, is worth over $200. But that’s a lot bulkier and heavier than two $100 bills.

If you’re looking to buy a significant amount of silver, say $25,000 or more, you’re going to be looking at a significant amount of bulk. That amount of cash will fit in a fanny pack or small purse.

That amount of gold will fit in a Ziploc bag in your pocket. But that amount of silver might require a decently sized briefcase or small suitcase.

Keep that in mind when you’re considering silver vs. cash, or silver vs. gold vs. cash.

Is Silver or Cash The Right Choice for You?

If you’re looking for a safe haven to park your money during an upcoming recession, there’s a good chance that you’re going to be choosing from among assets that include cash and silver. The ultimate decision about whether or not to buy silver or remain in cash is something that you’ll have to decide on based on your particular financial situation.

Whether to choose silver or cash could come down to how long you’ve been active in markets, how much longer you have until retirement, or how much money you’re looking to protect.

With silver, there is the potential for great gains during a recession, but there are no guarantees. And there will likely be periods of time where your silver holdings could sustain losses.

With cash, you’re guaranteed not to make losses, at least in nominal terms. But your cash holdings will lose purchasing power every year to inflation.

Cash can be easy to get, as easy as pulling money out of your bank account. And while silver does take a little more effort to acquire, with the help of experienced partners like Goldco the silver buying process can be quite simple.

Goldco has helped thousands of Americans benefit from owning silver. And with over 6,000 5-star reviews and over $5 billion in precious metals placements, we have worked hard to make ourselves one of the biggest and most trusted silver companies in the country.

If you’re wondering whether to choose silver vs. cash, contact the experts at Goldco today to learn more about the many benefits of buying silver.

The Indian government recently raised tariffs on gold and silver in response to a currency crisis, which could decrease Indian gold and silver demand Coinbase’s introduction of new...

Key Takeaways Prices for goods like housing, tuition, and oil appear to skyrocket or fluctuate wildly in dollars, but they often remain stable or even decrease when measured in gold Although...

When you’re looking for a place to live, do you look for the best house you can, or would you settle for a rundown hovel with broken windows, leaky faucets, and mice living in the walls When...

*Applies only to qualified orders. Get up to 5% back in FREE Gold or Silver when you purchase $50,000 – $99,999 in Goldco premium coins. Get 10% in FREE Gold or Silver when you purchase $100,000 or more in Goldco premium coins. Cannot be combined with any other offer. Additional rules may apply. Contact your representative to find out if your order qualifies. For additional details, please see your customer agreement. Goldco does not offer financial or tax advice regarding the purchase of precious metals.