The United States government’s national debt stands today at an astronomical $22.6 trillion. Everyone knows that’s a huge amount of money, but the sum is so large that it just boggles the mind and can be difficult to conceptualize. So here are a few ways of thinking about the national debt that will put it into perspective to help you realize just how large it is.

National Debt vs. GDP

The national debt now exceeds the entire gross domestic product of the United States, that is, the entire annual economic output of the country. Right now it’s at about 106% of GDP, which would mean that if the entire economic output of the country were redirected towards paying off the national debt, it would take over a year to complete.

Comparing the national debt to the world’s GDP of about $81 billion, we see that the US national debt is about 28% of the world’s total economic output. That’s pretty amazing when you think about it, that 535 men in Washington have managed to rack up a debt equal to 28% of the total annual work product of over 7.5 billion people.

National Debt vs. Federal Budget

The estimated federal budget for Fiscal Year 2020 is $4.746 trillion. The national debt is nearly five times that number. So much for paying down any part of the debt anytime soon.

National Debt vs. Income Tax Receipts

Some people may think that it’s no problem to pay off the national debt, just use tax receipts to do it. But income tax receipts for FY 2020 are expected to be around $1.822 trillion. That means that if every single dollar of income taxes received by the federal government were to go towards paying off the national debt, it would take over 12 years.

Even if you expanded that to include all government revenues, an estimated $3.643 trillion, it would take over six years to pay off the national debt. And that would mean no spending on Social Security, Medicare, defense, etc. for those six years.

National Debt vs. the World’s 10 Richest Men

The 10 richest men in the world have a combined estimated net worth of about $744 billion. That seems like a lot, until you compare it to the national debt. The US national debt is about 30 times the wealth of those 10 men combined.

National Debt in $100 Bills

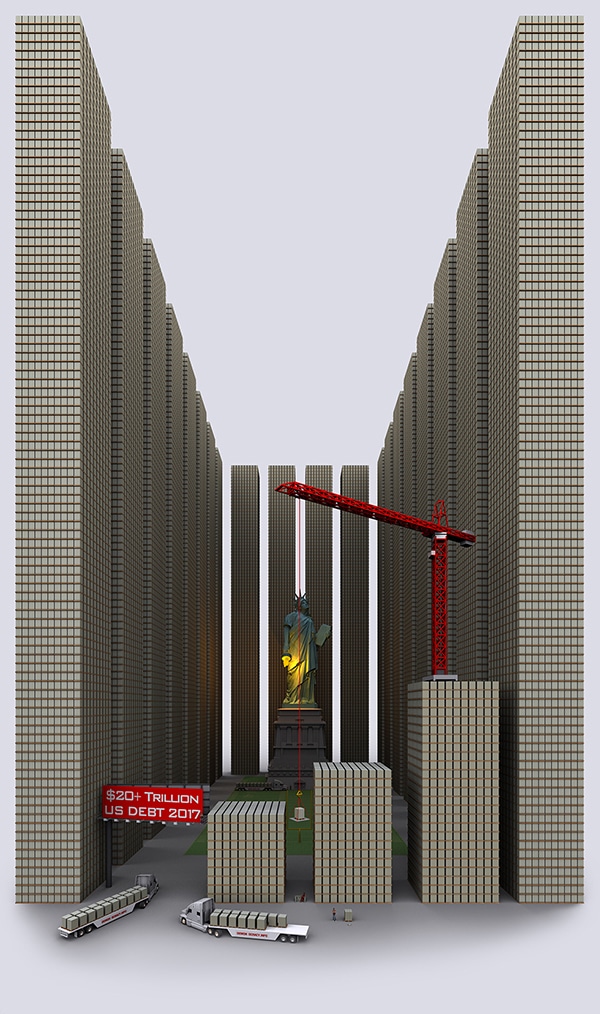

Here’s where visualization really can help. This image from Demonocracy really illustrates just how large the national debt problem is. The image is from 2017, when the national debt was a mere $20 trillion. Now the national debt is over 10% larger.

Each of those little squares is a pallet of $100 bills, worth about $100 million. And as you can see, packed 10×10 and then on top of each other, the national debt forms dozens of piles nearly twice as tall as the Statue of Liberty.

The Consequences of the National Debt

The national debt is no laughing matter, it’s a serious problem that has to be addressed. But no one in Washington takes it seriously. In fact, the government expects to continue adding over a trillion dollars each year to the national debt.

The effects of all that debt won’t be pretty, and it will be taxpayers, rather than the politicians who accumulated that debt, who will be left to pay the bill. Default is all but inevitable, which will destroy the dollar’s status as a reserve currency, if it isn’t already been lost by that point. Anyone invested in dollar-denominated assets like stocks and bonds will take a hit to their investments too.

That’s why the smart money is moving into gold to protect investor assets from the consequences of this massive national debt accumulation. Only by investing in gold can investors ensure that their assets remain safe in the face of a continually rising national debt.

Unless you’ve been living under a rock for the past few years, you’ve probably heard about artificial intelligence (AI) In fact, you’re probably sick of hearing about it, as AI has become a...

Oil and gas prices have risen significantly in the last few months as a result of the war against Iran Consumer and producer price indices have risen as a result, and there are fears that...

Key Takeaways Gold is no longer just reacting to Federal Reserve interest rate hikes or cuts; it is now pricing in the structural deterioration of sovereign balance sheets The US is currently...

*Applies only to qualified orders. Get up to 5% back in FREE Silver when you purchase $50,000 – $99,999 in Goldco premium coins. Get 10% in FREE Silver when you purchase $100,000 or more in Goldco premium coins. Cannot be combined with any other offer. Additional rules may apply. Contact your representative to find out if your order qualifies. For additional details, please see your customer agreement. Goldco does not offer financial or tax advice regarding the purchase of precious metals.